Most financial plans are designed to work.

They are built on reasonable assumptions, balanced inputs, and consistent projections.

Nothing in the structure appears fragile.

But planning is not tested on paper.

It is tested when conditions begin to shift.

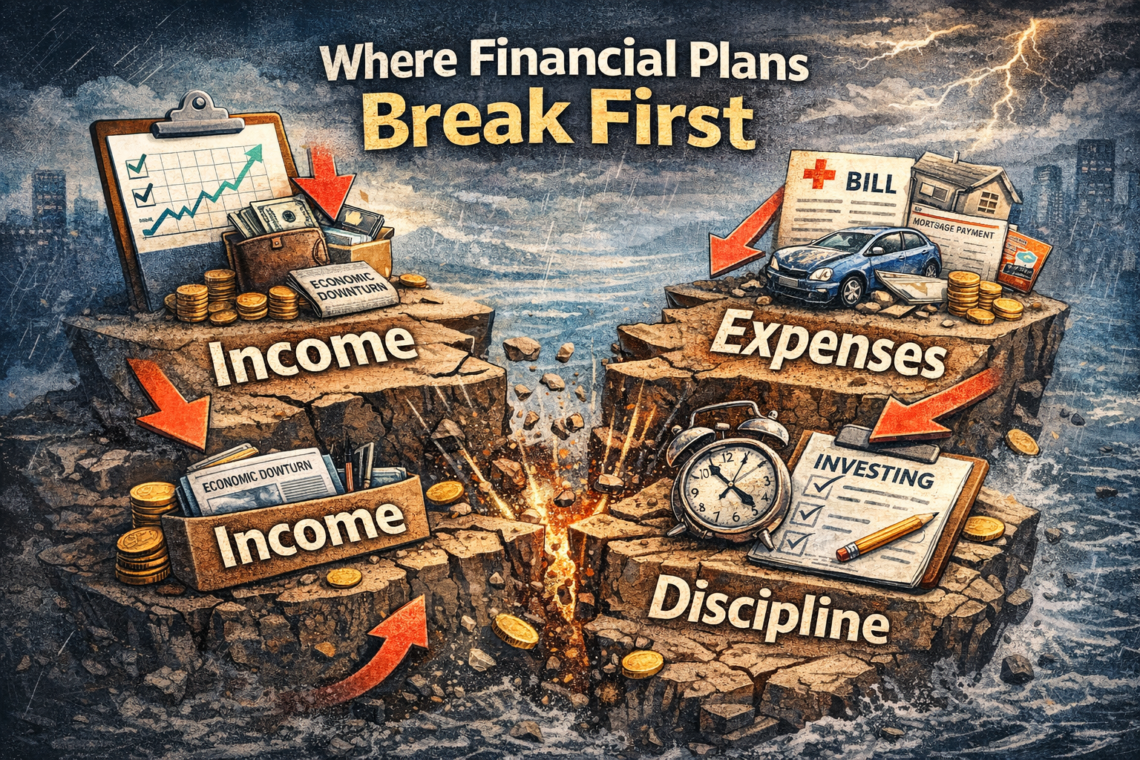

1) The Point Where Plans Are Tested

Most financial plans do not break at the end.

They are tested much earlier—when one part of the structure begins to shift.

On paper, the plan is balanced:

- Income supports expenses

- Expenses leave room for investing

- Investing compounds over time

The structure appears stable.

But real life does not apply pressure evenly.

It pushes on one part first.

And when that happens, the question is not whether the plan works.

It is which part breaks first.

2) Three Moving Parts, One Constraint

Every plan rests on three elements:

- Income — what comes in

- Expenses — what must go out

- Discipline — what is maintained over time

These are not independent.

They interact constantly, and pressure on one quickly transfers to the others.

- When income weakens, discipline is tested.

- When expenses rise, both income and discipline must compensate.

- When discipline slips, the structure loses stability even if income remains unchanged.

The plan does not fail all at once.

It begins to shift at its weakest point.

3) When Income Breaks First

Income is often assumed to be stable.

In reality, it can change:

- reduced hours

- career transitions

- business variability

- external economic conditions

When income drops, the plan must adjust immediately.

Expenses are rarely reduced at the same speed.

Investing is usually the first variable to move.

- Contributions shrink.

- Sometimes they pause.

Discipline does not disappear.

It is simply constrained by what is available.

4) When Expenses Break First

Expenses are often treated as predictable.

In practice, they are not.

- housing costs shift

- living expenses rise

- unexpected costs emerge

- lifestyle gradually expands

Unlike income, expenses tend to move quietly.

They do not announce themselves as a structural change.

They accumulate.

At first, the impact is small.

Then the margin begins to narrow.

- Investment contributions become tighter.

- Flexibility reduces.

Nothing appears broken.

But the plan is already under pressure.

5) When Discipline Breaks First

Discipline is often framed as a personal trait.

In reality, it is a function of structure.

When:

- income is unstable

- expenses are unclear

- surplus is inconsistent

discipline becomes difficult to maintain.

Missed contributions are not always behavioural.

They are often structural.

Consistency requires a system that can support it.

Without that, discipline is the first visible point of failure—even when it is not the original cause.

6) What This Reveals

These three elements do not fail independently.

One moves first.

The others follow.

- Income pressure reduces contributions

- Expense pressure reduces margin

- Structural pressure weakens discipline

What appears as a discipline problem is often:

an income or expense problem in disguise.

This is why plans that look balanced on paper can behave very differently in reality.

This becomes clearer when examining how income, expenses, and surplus interact through a

cost of living planning framework—where structure is measured, not assumed.

7) Why This Matters for Long-Term Independence

Financial independence is not determined by a single variable.

It depends on whether the structure can absorb pressure without breaking.

If one part fails early:

- contributions become inconsistent

- compounding weakens

- timelines extend

The outcome does not collapse.

It drifts.

Independence is not lost in one event.

It is delayed through small, repeated adjustments.

8) A Practical Reflection

A plan does not need perfect conditions to succeed.

But it does need to withstand imperfect ones.

- Income will change.

- Expenses will shift.

- Discipline will fluctuate.

The question is not whether these happen.

It is whether the structure anticipates them.

Because in most cases, the first thing that breaks is not the plan itself.

It is the assumption that nothing will.

Disclaimer: This article is for general information only and is not financial advice. You are responsible for your own financial decisions.