The 50/30/20 rule reveals what most plans ignore.

Most investment plans appear stable—until they are tested by real life.

The issue is rarely the investment itself.

It is whether the plan can be sustained once income, expenses, and priorities begin to shift.

A plan that depends on uninterrupted contributions is not robust.

It assumes a level of consistency that real life rarely provides.

And when that consistency breaks, the plan does not fail immediately.

It adjusts, pauses, and gradually moves away from its original path.

This is where simple structures such as the 50/30/20 rule begin to matter—not as a rule to follow, but as a way to see whether a plan can hold under real conditions.

1) What Actually Sustains Investing

A typical plan often starts with ambition.

- “I will invest as much as possible.”

- “I will maximise contributions early.”

- “I will accelerate compounding.”

On paper, this works.

In practice, investing is not sustained by intention.

It is sustained by what remains after income meets expenses.

If that remaining portion is unstable, the plan becomes unstable with it.

2) Where Plans Quietly Break

A common mistake is not overestimating returns.

It is overestimating how much can be consistently invested.

A plan might assume:

- $2,000 per month invested

- uninterrupted for 10–15 years

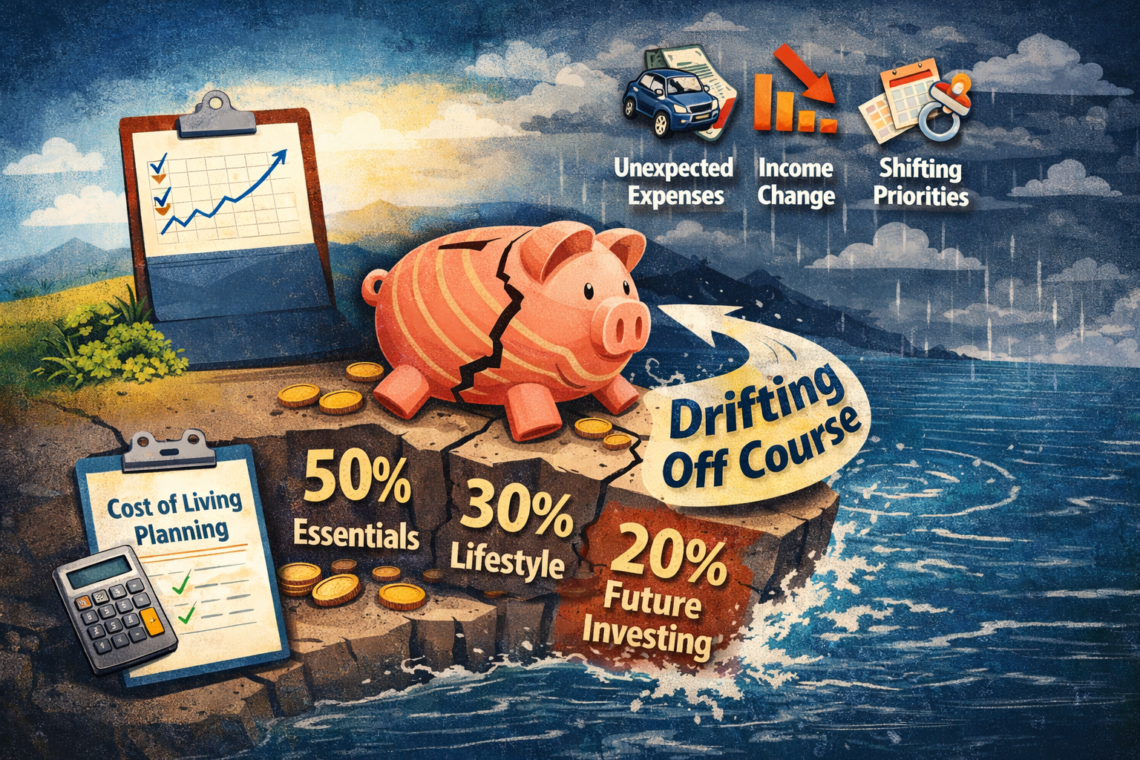

But real life introduces:

- unexpected expenses

- changes in income

- shifts in priorities

- periods of instability

When a plan is built on the maximum possible contribution, there is no room for these changes.

The result is not immediate failure.

It is gradual interruption.

Contributions are reduced.

Paused.

Sometimes stopped entirely.

The plan does not collapse.

It drifts.

The gap does not appear immediately.

It accumulates quietly.

3) The Starting Point Most People Skip

Before investing begins, there is a more basic requirement:

Understanding your own income and cost structure.

Not estimated.

Not approximated.

Measured.

This is where many plans remain incomplete.

Without a clear structure of:

- fixed expenses

- variable spending

- true surplus

investment decisions are based on assumptions rather than capacity.

This is why examining how income translates into actual investable surplus through a cost of living planning framework matters.

Not to optimise spending.

But to make the starting point visible.

4) A Simple Structure: 50 / 30 / 20

One widely used way to frame this is:

- 50% — Fundamentals (housing, food, transport, essential bills)

- 30% — Living (lifestyle, social, discretionary spending)

- 20% — Future (investing, saving, long-term planning)

This is not a rule to follow precisely.

It is a way to see structure.

It separates:

- what must be paid

- what can be adjusted

- what builds the future

5) Why This Structure Is Not Fixed

In reality, these categories shift.

The 30% (living) and 20% (future) portions are not fixed.

They move depending on:

- life stage

- income stability

- personal priorities

At certain times, future allocation may increase.

At other times, living allocation may take precedence.

The structure adapts.

6) Even the “50%” Is Not Absolute

The “fundamental” category is often treated as fixed.

It is not.

It changes depending on:

- whether you live independently or with family

- the cost of the city you work in

- housing structure and obligations

What appears as a fixed base is, in practice, variable across individuals.

7) What Happens When There Is Room

In some cases, part of the “fundamental” allocation may not be fully used.

For example:

- living costs are lower than expected

- housing is shared or subsidised

- expenses are temporarily reduced

If 10% remains within that structure, the question is not what it should be used for.

It becomes a decision point.

That portion can be directed toward:

- building an emergency reserve

- increasing investment

- investing in skills or education

- supporting social or personal activities

There is no universal answer.

The allocation reflects the individual’s priorities and circumstances.

8) Where Plans Become Real

A plan becomes viable not when it is maximised, but when it is aligned with how life actually operates.

When income, expenses, and surplus are clearly understood:

- contributions become consistent

- adjustments become manageable

- interruptions become less disruptive

At that point, investment is no longer dependent on ideal conditions.

It becomes part of a structure that can be sustained.

And when a structure can be sustained, even an ordinary investment can produce a stable outcome over time.

Not because the asset was exceptional, but because the plan was built to hold.

A plan that can only exist under ideal conditions is not a plan.

It is a projection.

Disclaimer: This article is for general information only and is not financial advice. You are responsible for your own financial decisions.